Explore the report:

Firm Foundations of Growth: East Asia and Pacific Economic Update, April 2024

The East Asia and Pacific (EAP) region is growing faster than the rest of the world, but slower than before the pandemic. While recovering global trade and easing financial conditions will support regional economies, increased protectionism and policy uncertainty will dampen growth. Amid macroeconomic turbulence, strong microeconomic foundations are critical for longer-term growth. Firms play a pivotal role in driving productivity, but leading firms in the region are not fully leveraging new technologies. How can these firms catch up with global leaders? What can be done to spur productivity growth?

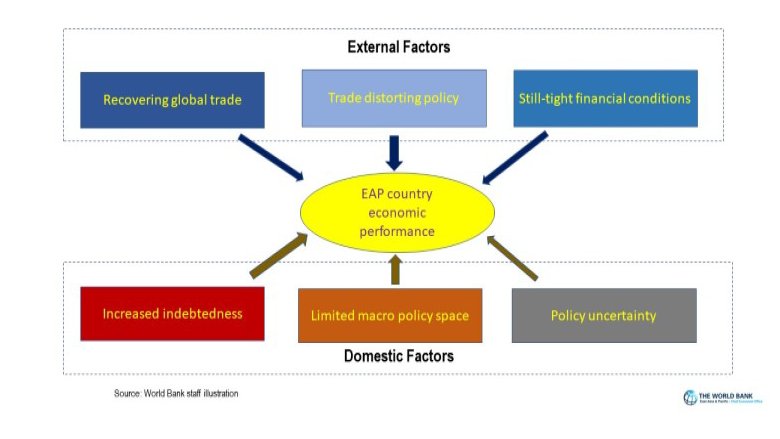

Most economies in developing East Asia and Pacific (EAP), other than several Pacific Island Countries, are growing faster than the rest of the world, but slower than before the pandemic. Economic performance in the region is being shaped by both external and domestic developments.

Read this section of the report:

|

The EAP region suffered in 2023 from slowing global growth and tightening financial conditions but is now expected to grow in 2024. The projected growth remains higher than that of other emerging markets and developing economies. Growth in China is projected to slow.

Read this section of the report:

|

In recent decades, EAP economic growth surpassed that in most other emerging market and developing economies in recent years, but this trend was driven primarily by capital accumulation rather than productivity growth. Firms play a critical role in driving productivity and while the productivity slowdown has been global, in advanced economies frontier firms continue to grow rapidly. In developing EAP however, it is the lagging firms that are catching up, while frontier firms are falling behind and are not fully leveraging new technologies.

Read this section of the report:

|

Policy Issues examined in recent economic updates

Previous updates have focused on a number of other policy issues, including:

(1) to contain COVID-19;

(2) for relief, recovery, and growth;

(3) to build back better;

(4) of COVID-19, especially through non-pharmaceutical interventions like testing-tracing-isolation;

(5) to prevent long-term losses of human capital, especially for the poor;

(6) to help households smooth consumption and workers reintegrate as countries recover;

(7) to prevent bankruptcies and unemployment, without unduly inhibiting the efficient reallocation of workers and resources;

(8) to support relief and recovery without undermining financial stability;

(9) , especially of still-protected services sectors��finance, transport, communications��to enhance firm productivity, avert pressures to protect other sectors, and equip people to take advantage of the digital opportunities whose emergence the pandemic is accelerating;

(10) creating and to promote equitable growth;

(11) policies to encourage ; and

(12) policies to address new and old .

(13) Policies to face up to the major (14) Policies to harness the to drive economy-wide growth and job creation.