Improving SMEs�� access to finance and finding innovative solutions to unlock sources of capital.

Overview

Small and Medium Enterprises (SMEs) play a major role in most economies, particularly in developing countries. SMEs account for the majority of businesses worldwide and are important contributors to job creation and global economic development. They represent about 90% of businesses and more than 50% of employment worldwide. Formal SMEs contribute up to 40% of national income (GDP) in emerging economies. These numbers are significantly higher when informal SMEs are included. According to our estimates, 600 million jobs will be needed by 2030 to absorb the growing global workforce, which makes SME development a high priority for many governments around the world. In emerging markets, most formal jobs are generated by SMEs, which create 7 out of 10 jobs. However, access to finance is a key constraint to SME growth, it is the second most cited obstacle facing SMEs to grow their businesses in emerging markets and developing countries.

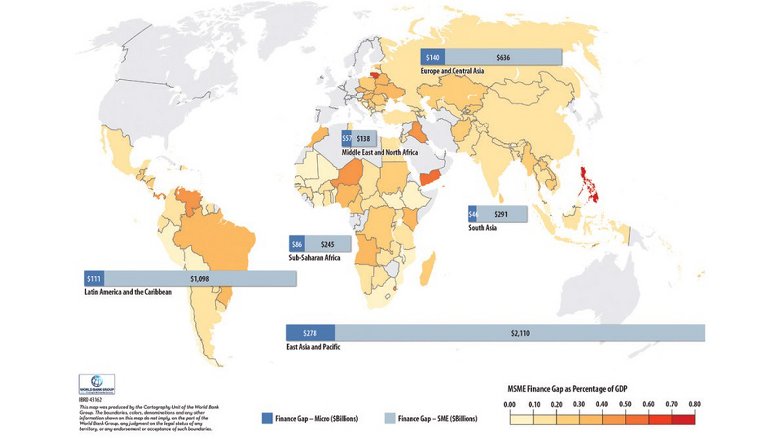

SMEs are less likely to be able to obtain bank loans than large firms; instead, they rely on internal funds, or cash from friends and family, to launch and initially run their enterprises. The International Finance Corporation (IFC) estimates that 65 million firms, or 40% of formal micro, small and medium enterprises (MSMEs) in developing countries, have an unmet financing need of $5.2 trillion every year, which is equivalent to 1.4 times the current level of the global MSME lending. East Asia And Pacific accounts for the largest share (46%) of the total global finance gap and is followed by Latin America and the Caribbean (23%) and Europe and Central Asia (15%). The gap volume varies considerably region to region. Latin America and the Caribbean and the Middle East and North Africa regions, in particular, have the highest proportion of the finance gap compared to potential demand, measured at 87% and 88%, respectively. About half of formal SMEs don��t have access to formal credit. The financing gap is even larger when micro and informal enterprises are taken into account.

Formal MSME Finance Gap in Developing Countries

What We Do

A key area of the World Bank Group��s work is to improve SMEs�� access to finance and find innovative solutions to unlock sources of capital.

Our approach is holistic, combining advisory and lending services to clients to increase the contribution that SMEs can make to the economy including underserved segments such as women owned SMEs.

Advisory and Policy Support for SME finance mainly includes diagnostics, implementation support, global advocacy and knowledge sharing of good practice. For example we provide;

Financial sector assessments to determine areas of improvement in regulatory and policy aspects enabling increased responsible SME access to finance

Implementation support of initiatives such as development of enabling environment, design and set up of credit guarantee schemes

Improving credit infrastructure (credit reporting systems, secured transactions and collateral registries, and insolvency regimes) which can lead to greater SME access to finance.

Introducing innovation in SME finance such as e-lending platforms, use of alternative data for credit decisioning, e-invoicing, e-factoring and supply chain financing.

Policy work, analytical work, and other Advisory Services can also be provided in support of SME finance activities.

Advocacy for SME finance at global level through participating and supporting G20 Global Partnership for Financial Inclusion, Financial Stability Board, International Credit Committee for Credit Reporting on SME Finance related issues.

Knowledge management tools and flagship publications on good practice, successful models and policy frameworks

Lending Operations:

SME Lines of Credit provide dedicated bank financing �C frequently for longer tenors than are generally available in the market �C to support SMEs for investment, growth, export, and diversification.

Partial Credit Guarantee Schemes (PCGs) �C the design of PCGs is crucial to SMEs�� success, and support can be provided to design and capitalize such facilities.

Early Stage Innovation Finance provides equity and debt/quasi-debt to start up or high growth firms which may otherwise not be able to access bank financing.

Results of Our Work

Early-Stage SME Finance

In Lebanon, the Innovative Small and Medium Enterprises (iSME) project is a $30 million investment lending operation providing equity co-investments in innovative young firms in addition to a grant funding window for seed stage firms. As of August 2019, iSME��s co-investment fund has invested $10.23 million across 22 investments and has been able to leverage $25.47 million in co-financing, demonstrating its ability to crowd in private sector financing and expand the market for early stage equity finance in Lebanon. To date, 60 out of 174 grantees had leveraged the iSME funding to raise a total of $13.1 million from various funding sources, a leverage ratio of 5.3 times. Overall, stakeholders�� consultations suggest that the iSME project could play an even larger role in the future financing of the Venture Capital (VC) sector by supporting existing VCs and emerging players, including increasing attention on a fund of funds approach, which could also cover growth funds (later stage and private equity).

In India, our MSME Growth, Innovation and Inclusive Finance Project improved access to finance for MSMEs in three vital but underserved segments: early stage/startups, services, and manufacturing. A credit line of $500 million, provided to the Small Industry Development Bank of India (SIDBI), was designed to provide an affordable longer-term source of funding for underserved MSMEs. Technical assistance of about $3.7 million complemented the lending component and focused on capacity building of SIDBI and the participating financial institutions (PFIs). In addition to directly financing MSMEs, disbursing a total of $265 million in loans, the project pushed the frontiers of MSME financing through the development of innovative lending methods that reduced turnaround time, reached more underserved MSMEs, and crowded in more private sector financing. It also reached new clients, women-owned MSMEs, and MSMEs in low-income states. The project supported SIDBI to scale-up of the Fund of Funds for Startups, which aims to indirectly disburse $1.5 billion to startups by 2025. SIDBI��s ��contactless lending�� platform, a digital MSME lending aggregator and matchmaking platform, has crowded in $1.9 billion of private sector financing for MSMEs, making it the largest online lender in India.

Lines of Credit

In Jordan, two World Bank Group��s lines of credit aim to increase access to finance for MSMEs and ultimately contribute to job creation. The $70 million line of credit encouraged the growth and expansion of new and existing enterprises, increasing outreach to MSMEs, 58% of which were located outside of Amman and 73% were managed by women. The line of credit directed 22% of total funds to start-ups. The project financed 8,149 MSMEs, creating 7,682 jobs, of which 79% employed youth and 42% hired women. The additional financing of $50 Million is progressing well towards achieving its intended objective. $45.2 million has been on-lent to 3,345 MSMEs through nine participating banks. The project is especially benefiting women, who represent 77% of project beneficiaries, and youth (48% of project beneficiaries), and increasing geographical outreach, as 65% of MSMEs are in Governorates outside of Amman.

In Nigeria, the Development Finance Project supports the establishment of the Development Bank of Nigeria (DBN), a wholesale development finance institution that will provide long-term financing and partial credit guarantees to eligible financial intermediaries for on-lending to MSMEs. The project also includes technical assistance to DBN and participating commercial banks in support of downscaling their operations to the underserved MSME segment. As of May 2019, the Development Bank of Nigeria credit line to PFIs for on-lending to MSMEs has disbursed US$243.7 million, reaching nearly 50,000 end-borrowers, of which 70% were women, through 7 banks and 10 microfinance banks.

Partial Credit Guarantees

In Morocco, the MSME Development project aimed to improve access to finance for MSMEs by supporting the provision of credit guarantees by enabling the provider of partial credit guarantees in the Moroccan financial system to scale up its existing MSME guarantee products and introduce a new guarantee product geared towards the very small enterprises (VSEs). As a result of the project, the number and volume of MSME loans are estimated to have increased by 88% and 18%, respectively, since the end of 2011. Cumulative volume of loans backed by the guarantees during the life of the project is estimated at $3.28 billion. With significantly increased lending supported by guarantees, PFIs were able to continue building their knowledge of MSME customers, refining their systems to serve them more effectively and efficiently. Owing to guarantees, many first-time borrowers were able to generate credit history, which made it easier for them to obtain loans in future.

Supporting Women-Owned SMEs

In Ethiopia, the Women Entrepreneurship Development Project (WEDP) is an IDA operation providing loans and business training for growth-oriented women entrepreneurs in Ethiopia. After identifying a persistent ��missing middle�� financing gap for women entrepreneurs in Ethiopia, WEDP launched as a microfinance institutions�� (MFIs) upscaling operation, helping Ethiopia��s leading MFIs introduce larger, individual-liability loan products tailored to women entrepreneurs. WEDP loans are complemented through provision of innovative, mindset-oriented business training to women entrepreneurs. As of October 2019, more than 14,000 women entrepreneurs took loans and over 20,000 participated in business training provided by WEDP. 66% of WEDP clients were first-time borrowers. As a result of the project, participating MFIs increased the average loan size by 870% to $11,500, reduced the collateral requirements from an average of 200% of the value of the loan to 125%, and started disbursing $30.2 million of their own funds as WEDP loans. The average WEDP loan has resulted in an increase of over 40% in annual profits and nearly 56% in net employment for Ethiopian women entrepreneurs.

In Bangladesh, the Access to Finance for Women SMEs Project aims to create an enabling environment to expand access to finance to women SMEs (WSME) by supporting the establishment of credit guarantee scheme (CGS), issuance of SME Policy, and strengthening capacity of the regulator and sector. The project supported the issuance of Bangladesh��s maiden SME Policy. Bangladesh��s first comprehensive SME Policy was launched in December 2019 through concerted efforts in high-level upstream work, enhancement of the regulator��s capacity, and formulation of key recommendations with a sharper gender lens. In Bangladesh, $2.8 billion financing gap prevails in the MSME sector, where 60% of women SME��s financing needs are unmet, and lack of access to collateral is one of the key hindrances. Bangladesh lacked a single policy with systemic plan to enhance SME finance. With nearly 10 million SMEs contributing to 23% of the GDP, 80% of jobs in the industries sector and 25% of the total labor force, the SME Finance Policy will play a pivotal role in enhance SME financing.

Leasing

In Ethiopia and Guinea, the World Bank Group is supporting the local governments in creating an enabling framework which is conducive to launching and growing leasing operations, as well as attracting investors, to increase access to finance for SMEs. It is doing so by working at the macro, mezzo, and micro levels, supporting the governments with legal and regulatory reforms, and working with industry players to create technical partnerships and increase market awareness and capacity. In Ethiopia, the project generated a $200 million credit facility supporting 7 leasing intuitions and introducing 4 new leasing products into the market: hire purchase, finance lease, microleasing and agrileasing. As of June 2019, 7,186 MSMEs have accessed finance valued at over $147 million. The project in Guinea supported the adoption of the national leasing law and the accompanying prudential guidelines for leasing, which in turn, have helped 3 companies to launch leasing operations. To date, these institutions have supported 31 SMEs through the disbursement of leases valued at $25 million.

Who We Work With

Leveraging our expert knowledge, we work globally with public stakeholders and private sector intermediaries in partnership with other multilateral and bilateral development organizations to support SME Finance development in emerging markets and developing countries.

This site uses cookies to optimize functionality and give you the best possible experience. If you continue to navigate this website beyond this page, cookies will be placed on your browser. To learn more about cookies, click here.